TL;DR

Kubera and Capitally both track wealth for self-directed investors with complex portfolios, but they are built on opposite philosophies. Kubera is a net-worth balance sheet: connect your accounts through aggregators, see today's number, and pay one flat $250/year regardless of portfolio size. Capitally is a transaction-level portfolio analyzer: upload broker statements, keep the full history, and get on-device end-to-end encryption, professional-grade analytics and multi-jurisdiction tax reporting from €80/year.

- Choose Kubera for hands-off automated balance sync, automatic valuation of illiquid assets, and estate-handover features — at a flat price.

- Choose Capitally for data privacy, a complete transaction history that holds up at tax time, and deep analytics across any asset class.

Table of Contents

- TL;DR

- Is Kubera safe? Privacy and data security

- Balance sheet vs transaction ledger

- Tracking real estate, private equity and alternative assets

- Performance analytics and reporting

- Multi-currency support and FX attribution

- Dividends and investment income

- Tax reporting and cost basis

- Options and liabilities

- Multiple portfolios and entity structures

- Pricing

- Moving from Kubera to Capitally

- Which should you choose?

- Common questions about Kubera and Capitally

Here is the head-to-head at a glance:

Feature | Kubera | Capitally |

|---|---|---|

Pricing | $250/year flat (Essentials); $2,500/year (Black) | €80 (Sailor), €130 (Navigator), €250/year (Captain) |

Free trial | 14-day trial; no free plan | 14-day trial, no credit card; no free plan |

Data model | Current balances only — no transaction ledger | Full transaction history from broker statements, or balances only |

Broker data | Automated balance sync via 9 aggregators (Plaid, Yodlee, MX, SnapTrade and more) | Manual statement import from 70+ brokers; no aggregators by design |

Privacy | Encryption in transit and at rest; data readable on Kubera's servers | On-device end-to-end encryption; even Capitally cannot read your data |

Asset classes | Stocks, ETFs, bonds, funds, crypto/DeFi/NFT, real estate, vehicles, private equity, collectibles | Stocks, ETFs, bonds, funds, crypto, real estate, private equity, options, loans, P2P, art, any custom asset |

Options | ❌ Not supported | Full option strategies with Greeks (Captain plan) |

Liabilities | Manual, balance-only | First-class loans and mortgages with interest accrual and amortization |

Multi-currency | View in a fixed currency list plus BTC; no FX attribution | Mix any currencies; separates currency return from capital return |

Tax reporting | ❌ Manual cost basis plus a rough tax estimate | Capital-gains presets for ~11 jurisdictions; six cost-basis methods; tax-loss harvesting |

Analytics | Net-worth trends, allocation pies, Sankey cash-flow, IRR | TWR, MWR, IRR, ROI; pivot-style Portfolio Explorer; 10 benchmarks; real (inflation-adjusted) returns |

Multiple portfolios | Single portfolio on Essentials; nested entities need the $2,500 Black plan | Multiple projects and nested accounts from Navigator up |

AI features | AI Import, AI Appraiser, Recap, MCP access for ChatGPT/Claude/Perplexity | By design, none — on-device encryption rules out server-side AI |

Platforms | Web app and mobile PWA; no native apps, online only | Web app and mobile PWA, fully offline-capable |

Best for | Hands-off net-worth tracking, illiquid-asset valuation, estate handover | Privacy, complete history for tax, deep analysis of complex multi-asset portfolios |

Managing wealth as a high-net-worth investor means holding more than stocks and bonds — private equity, real estate, alternatives, multiple entities, several currencies. The real question is not whether a tool can show your net worth, but how it gets there and what it lets you do with the data afterward.

Kubera, founded in 2019, is a net-worth balance sheet: it aggregates account balances into a clean, current picture. Capitally, launched in 2023, is a transaction-level portfolio analyzer: it records the full history behind every position, so you can measure performance, file taxes, and stress-test your allocation. Both target sophisticated investors. They disagree on how your financial data should be handled, and on how much analysis you actually need.

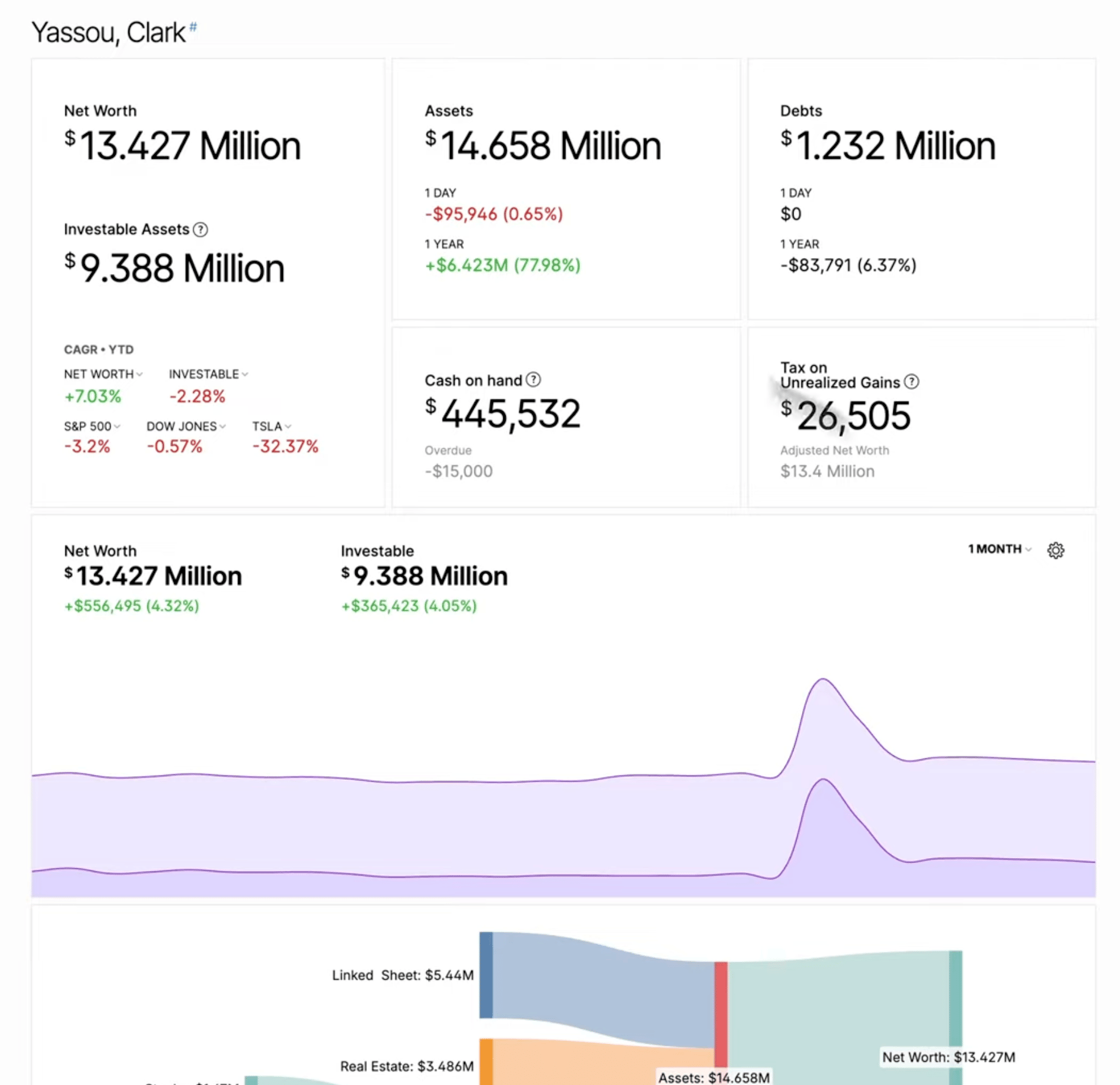

Kubera dashboard

Kubera dashboard Capitally dashboard

Capitally dashboardIs Kubera safe? Privacy and data security

Capitally is the more private of the two platforms. It uses on-device end-to-end encryption: your financial data is encrypted with a key derived from your password that never leaves your device, so even Capitally cannot read it. Kubera uses standard security — encryption in transit and at rest — but your data is readable on its servers, and its account sync depends on third-party aggregators.

To sync accounts, Kubera connects through nine aggregators (Plaid, Yodlee, MX, SnapTrade, Akoya and others), with a router that picks the best one per institution. For open-banking institutions your credentials go to the bank's own OAuth page; for the rest they are entered on the aggregator's screen. Kubera adds two-factor authentication, and applies end-to-end encryption to documents you upload. It is a reasonable mainstream security model — but it still means your unencrypted balances live on company servers, your financial data goes through a third-party, and SOC 2 certification covers only Kubera's business and white-label tiers, not the consumer plans.

Kubera has also repositioned around AI, with the tagline "Works for you. Works for your AI." Its MCP integration exposes your portfolio to ChatGPT, Claude, Perplexity and other assistants in near-real-time, and AI Import reads documents and screenshots for you. The convenience is real. So is the trade: every AI integration needs your portfolio readable on a server it can call, which is exactly what end-to-end encryption protects you from.

Capitally has made the opposite trade. There are no AI integrations and no aggregator connections — and there cannot be, because the on-device encryption that keeps your data unreadable to Capitally also keeps it unreadable to any AI agent or third-party service. Calculations run locally; servers are hosted in Europe on Google Cloud (GDPR by design); there are no ads or third-party trackers; you can export everything at any time.

The honest trade-off: if you want automation and accept that your data lives, readable, on a vendor's servers and flows through aggregators, Kubera's model is a fair deal. If you treat data exposure as the thing to minimize, Capitally's on-device encryption is the stronger fit.

Balance sheet vs transaction ledger

This is the structural difference everything else follows from. Kubera tracks current balances — a snapshot of what each account is worth today, with no underlying transaction ledger. Capitally records every transaction — buys, sells, dividends, fees, FX conversions, corporate actions — so it can reconstruct cost basis, realized and unrealized profit, and returns over any period.

Kubera's aggregators sync balances, not transaction detail. If a connection drops for a week, you re-enter the change manually. You can record cash flows per asset to get an IRR figure, but there is no portfolio-wide ledger and limited ability to correct the past. For a pure net-worth snapshot, this is fast and low-maintenance — which is the point.

Capitally imports broker statements that typically reach back to the day the account was opened, with every corporate action, dividend reinvestment and FX conversion intact — exactly the data that lot-level cost basis and a defensible tax filing depend on. A Project History page lets you search every change, audit a single asset's edit history, and revert the whole project to any earlier point.

The honest trade-off: if all you want is "what am I worth today," Kubera's model is enough and less work. If you need to know your real return, or file taxes from your own records, the transaction ledger is not optional.

Tracking real estate, private equity and alternative assets

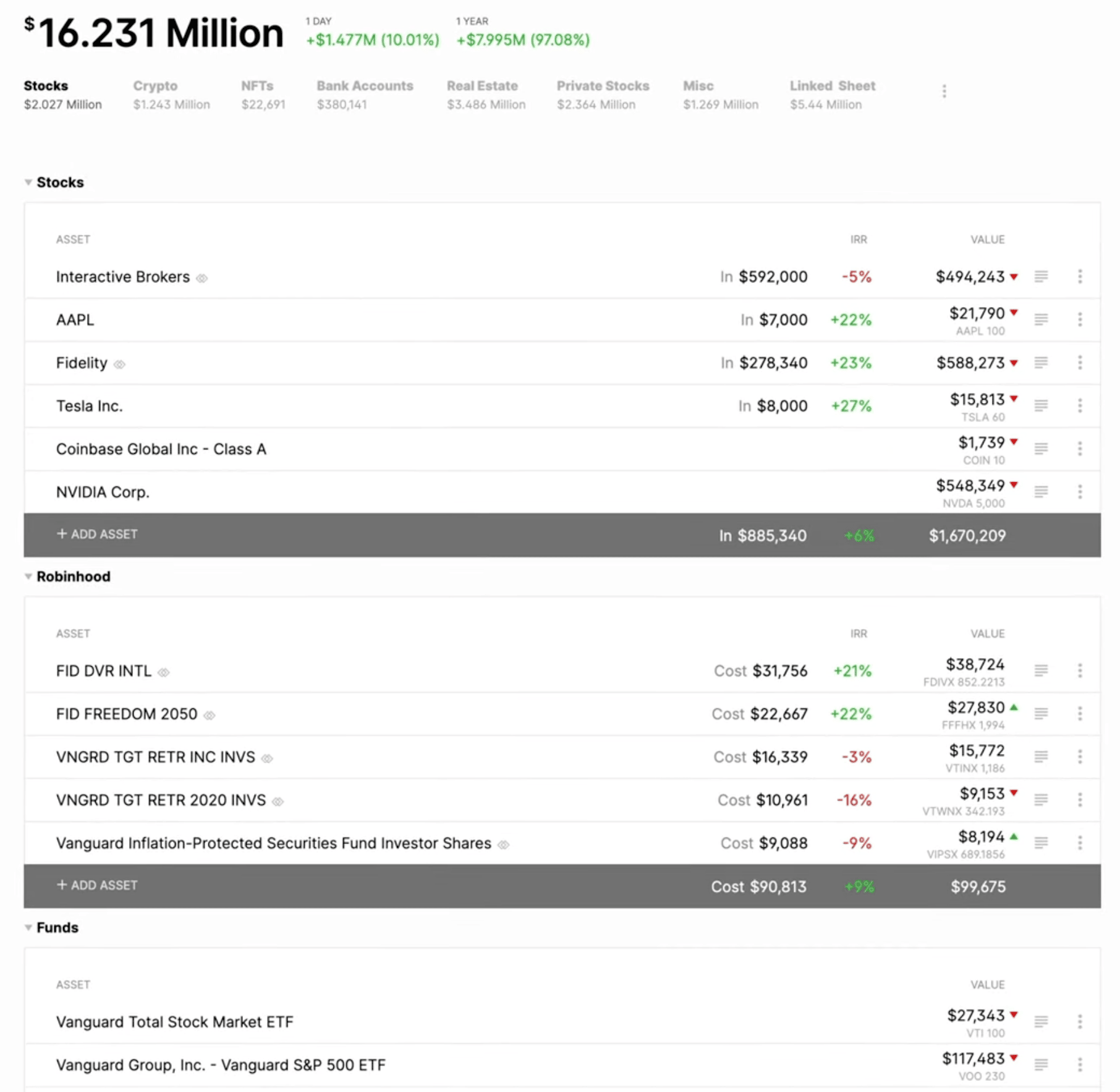

Both platforms handle alternative assets well, with different strengths. Kubera automates valuation of hard-to-price holdings — art, jewelry, watches, vehicles, collectibles — through its AI Appraiser, pulls US property values from Zillow, and integrates directly with Carta for private-equity and startup positions. Capitally tracks a wider range of asset classes — including options, loans, mortgages, P2P loans and derivatives — and lets each carry rental income, related liabilities and full transaction history, rather than only a current value.

Private equity is a good example. Both track it with capital calls and distributions. Kubera does it through its Carta integration — convenient if your fund is on Carta. Capitally has a dedicated private-equity asset type covering the full limited-partner lifecycle — commitments, calls, distributions and NAV — alongside managed, black-box holdings priced from NAV and cash flows. Custom-asset prices can be imported, not only typed in.

Where they diverge: Kubera's AI Appraiser is genuinely novel for hard-to-value objects, and its valuations update over time. Capitally instead lets each alternative asset carry rental income, related liabilities and full performance history — real estate with rental income and a mortgage attached, P2P loans with interest receipts, ventures with their own cash-flow record — across roughly 400,000 indexed instruments plus any custom asset you define.

The honest trade-off: Kubera is the easier path if your alternatives are mostly things AI Appraiser or Carta can value for you. Capitally is the deeper path if you want those assets to behave like any other holding — with income, liabilities and history.

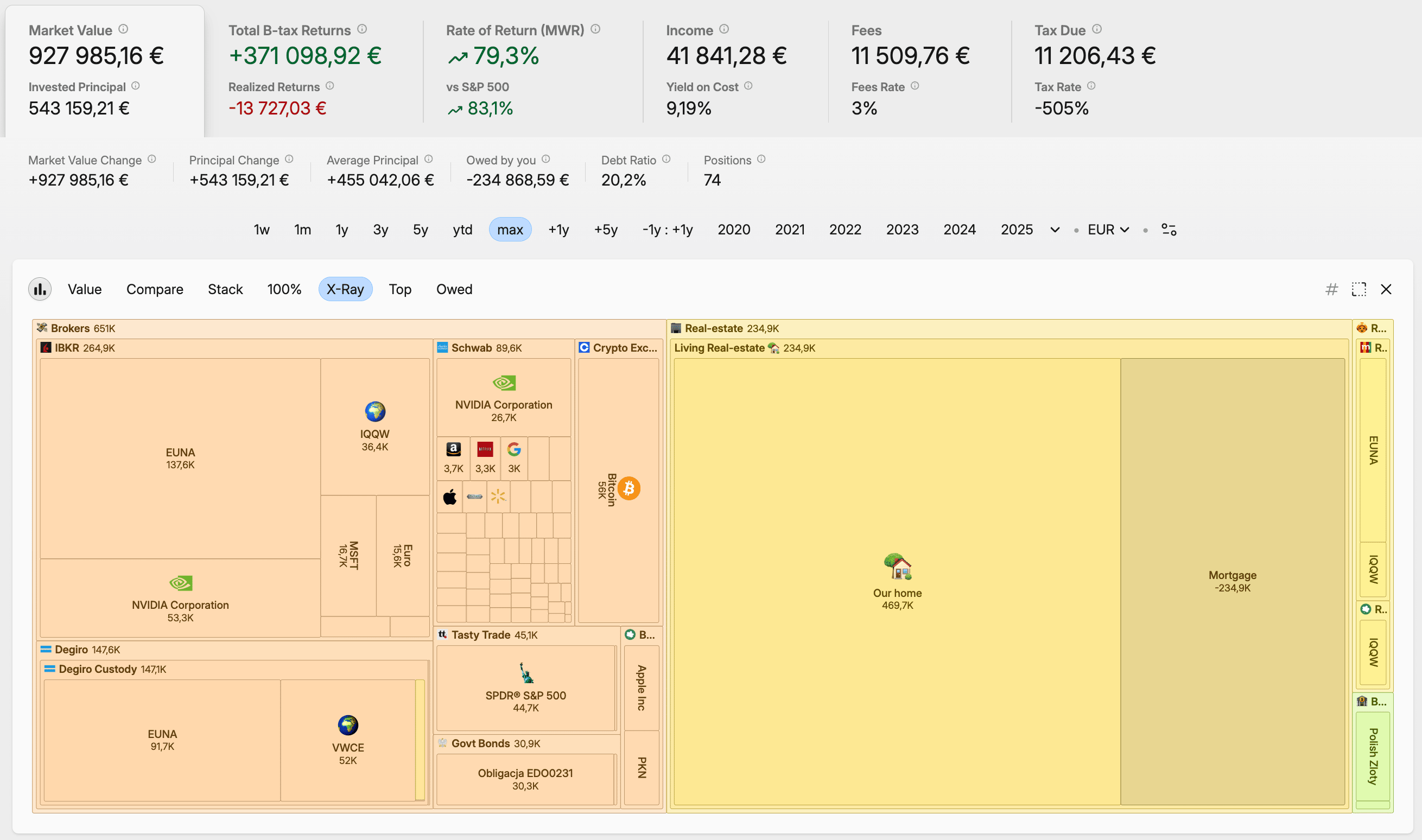

Performance analytics and reporting

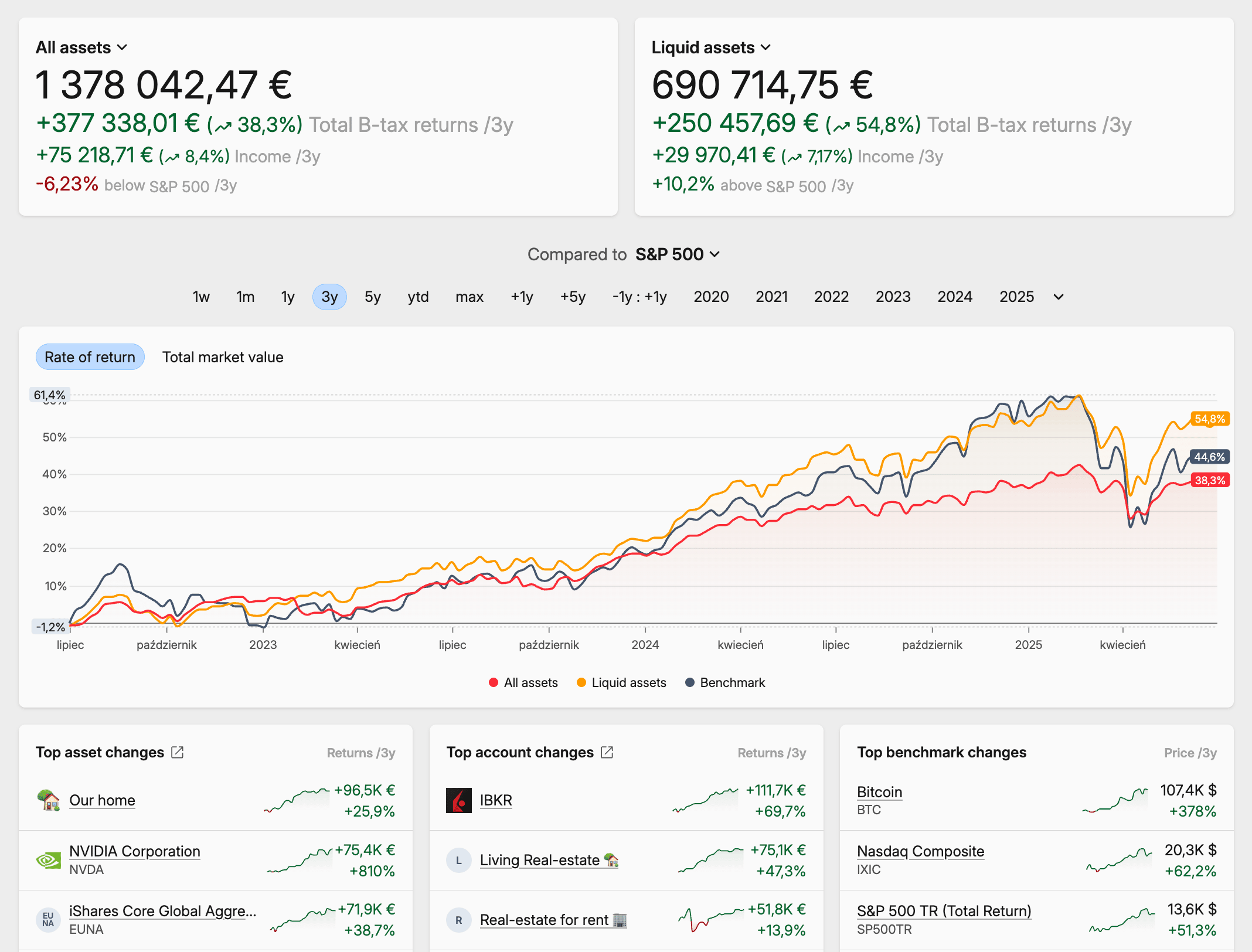

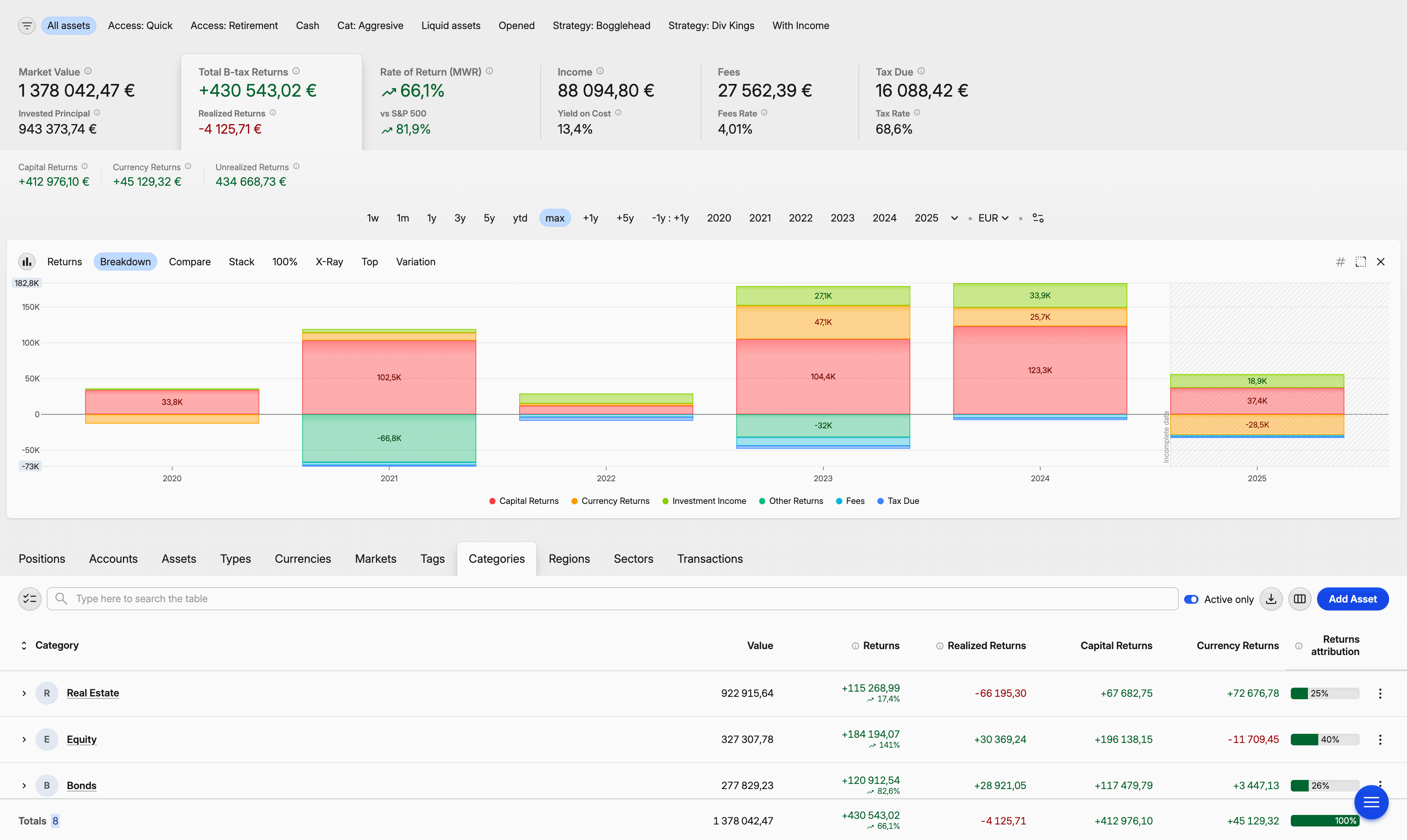

Capitally is built for analysis; Kubera is built for an overview. Capitally calculates time-weighted return (TWR), money-weighted return (MWR/IRR) and ROI, and its Portfolio Explorer works like a pivot table joined to a pivot chart — filter, group and chart any slice of the portfolio over any period. Kubera keeps reporting deliberately simple: net-worth trends, allocation pie charts, a Sankey cash-flow diagram and an IRR figure.

Kubera's reporting matches its overall approach — clean, uncluttered, enough to monitor overall wealth. It includes a "Fast Forward" projection (enter assumed growth rates and future cash flows to chart a possible trajectory) and Club Benchmarks, which compares your allocation and performance against an anonymized aggregate of Kubera users with a similar net worth. Peer benchmarking like that is genuinely uncommon, and useful if you want a sense of how you stack up.

Capitally goes deeper. Time-weighted return strips out the effect of when you added money — useful for judging your strategy; money-weighted return keeps your timing in — useful for judging your decisions. On top of that: custom charts, up to 10 benchmarks plotted at once, built-in economic indicators (CPI, policy rates, house-price indices) usable as benchmarks, and a "discount-by" option that shows real, inflation-adjusted returns. A Position-Prices benchmark answers "what would I have if I had never traded."

The honest trade-off: Kubera answers "how is my wealth trending." Capitally answers "which of my decisions worked, and why."

Kubera assets overview

Kubera assets overview Capitally portfolio analysis

Capitally portfolio analysisMulti-currency support and FX attribution

Capitally has the stronger multi-currency model. It lets transactions, prices and fees mix currencies, switches your viewing currency at any time, and — the part that matters most — separates currency return from capital return, so you can see whether an international position made money on the asset itself or on the exchange rate. Kubera shows your portfolio in a fixed list of currencies (plus Bitcoin), but does not break down FX impact.

For an investor holding a single currency, this barely registers. For expat and multi-broker investors holding two or more, FX attribution changes the picture: a "good year" in your base currency can be a flat year in the asset's local currency, with all the move coming from the exchange rate.

Dividends and investment income

Capitally tracks investment income in detail; Kubera does not. Capitally imports dividends from broker statements with withholding-tax data, handles dividend reinvestment (DRIP) and stock dividends, splits distributions into taxable and return-of-capital portions, and reports yield, yield-on-cost, growth rates and a forward dividend calendar. Kubera treats dividends as ordinary cash flow — no dividend reports, DRIP handling, forecasting or withholding-tax tracking.

If you do not manage for income, Kubera's omission will not bother you. If dividends, rent or bond interest are part of your plan, Capitally's income tooling is a real difference — and it extends the same treatment to rental income, P2P lending returns and staking rewards.

Tax reporting and cost basis

Capitally is an actually useful tax tool. It has built-in capital-gains presets for more than eleven jurisdictions, six cost-basis methods — FIFO, LIFO, Highest Cost, Lowest Cost, Average Cost and manual lot selection — selectable per position, a tax-loss-harvesting view that shows how many shares to sell for a target benefit, and a dedicated tax report.

Kubera lets you enter a cost basis and a tax rate per asset for a rough estimate, with no country-specific rules, tax-year handling or harvesting.

Average Cost Basis in particular matters for Canadian, UK and many European investors, and it is a method most net-worth trackers skip. The honest trade-off: if you hand everything to an accountant and only need a ballpark figure, Kubera's estimate is a starting point. If you file from your own records, Capitally produces the underlying data to file from.

Options and liabilities

Capitally tracks options and liabilities as first-class positions; Kubera tracks neither. Capitally is one of the few personal portfolio trackers that handles full option strategies — calls, puts, covered calls, spreads, multi-leg positions — with Greeks (Delta, Gamma, Theta, Vega, Rho) and standard option-pricing models. It also treats loans and mortgages as first-class assets, with automatic interest accrual and amortization. Kubera does not track option contracts at all, and records liabilities as manual, balance-only entries.

Most net-worth trackers skip both — Kubera included. If you trade options, or want leverage and debt reflected accurately in your returns and net worth, that is a real gap on Kubera's side and Capitally fills it. If neither matters to you, it is not a factor. Note that options and margin sit on Capitally's Captain plan.

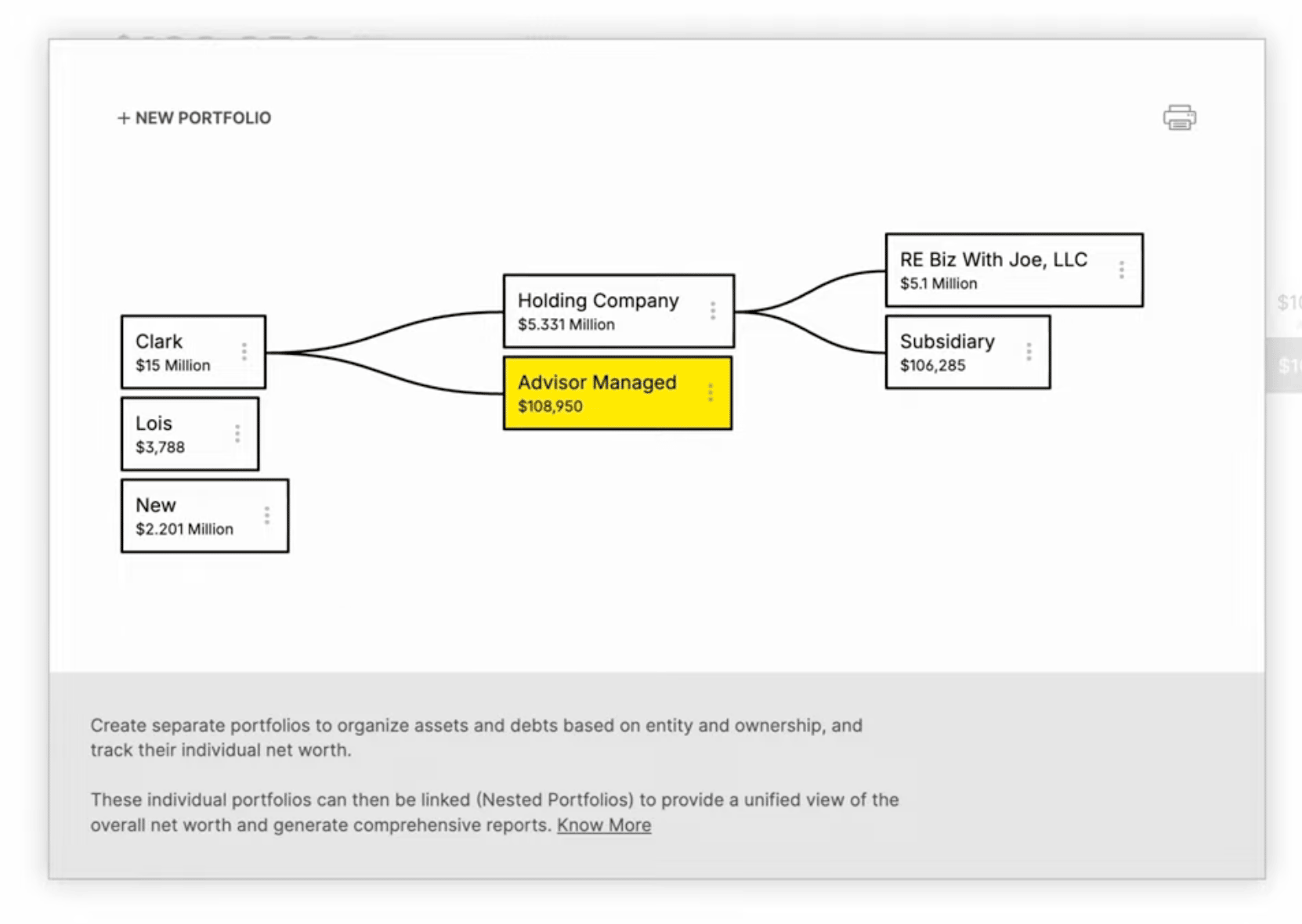

Multiple portfolios and entity structures

Both platforms handle multiple portfolios, but at very different price points. Capitally includes multiple projects and deeply nested accounts from its €130 Navigator plan, so you can separate legal entities, family members or test strategies. Kubera's base $250 Essentials plan is a single portfolio; nested portfolios for trusts, LLCs and family entities require the $2,500 Black plan.

Kubera Black does more than unlock nesting, though. It adds granular access control, concierge onboarding and full-access multiplayer sharing — genuinely built for family offices and advisor relationships where several people need controlled access to the same portfolio. Capitally has no multi-user access or granular permissions; its projects are designed for one person managing several structures.

The honest trade-off: for a single investor with a few entities, Capitally covers it for far less. For a household or family office that needs several people in one portfolio with controlled access, Kubera Black is purpose-built for that — at a price to match.

Kubera nested portfolios

Kubera nested portfolios Capitally nested accounts

Capitally nested accountsPricing

Kubera charges one flat price; Capitally charges by capability.

Kubera is $250/year for Essentials and $2,500/year for Black, regardless of portfolio size.

Capitally has three tiers — Sailor at €80, Navigator at €130, and Captain at €250 per year — with Captain adding private-equity tracking, options and margin. Both run a 14-day trial, and neither has a permanent free plan.

For most high-net-worth users the real comparison is Kubera Essentials ($250) or Black ($2,500) against Capitally Navigator (€130) or Captain (€250). Capitally Captain — its most complete plan — costs roughly a tenth of Kubera Black, and Capitally locks your price for the life of the subscription even if list prices rise.

The honest trade-off: Kubera's flat price is genuinely simple, and for a very large portfolio that needs multi-entity support and VIP service, $2,500 can be reasonable. For most investors, Capitally's plans deliver much more analysis for much less money.

Moving from Kubera to Capitally

Migrating is more straightforward than it sounds, because you do not move data out of Kubera at all — you import from your brokers. Kubera stores balances rather than a transaction history, so the cleaner path is to export statements from each broker and import those into Capitally, which rebuilds the full history automatically.

- Export account statements from each broker — most reach back to the day the account was opened.

- Import them into Capitally. Prices, dividends and splits are filled in automatically; review and confirm the reconciliation of assets, accounts and currencies.

- For holdings with no broker statement — real estate, private equity, collectibles — create a custom asset and enter or import its valuation history.

- Save an import preset for each broker, so future updates take about a minute.

This is more work upfront than connecting an aggregator. The pay-off is that you end with a complete, verifiable history rather than a starting balance.

Which should you choose?

Choose the tool that matches how you want to work. Kubera is the better fit if you want a low-maintenance net-worth balance sheet, automated balance sync, automatic valuation of illiquid assets, and estate-handover features — all at one flat price. Capitally is the better fit if you want data privacy, a complete transaction history that holds up at tax time, and professional-grade analytics across stocks, options, real estate, private equity and liabilities.

Both run a 14-day trial. Given how differently they treat your data and your history, testing each with your real portfolio is the most reliable way to decide. To see how Capitally compares with other trackers, read our getquin review, Sharesight review and Snowball Analytics review.

Common questions about Kubera and Capitally

Kubera is worth it if you want a hands-off net-worth balance sheet and value its flat $250-a-year price, automated balance sync across nine aggregators, automatic valuation of illiquid assets, and estate-handover features. It is a weaker fit if you need a full transaction history, tax reports, dividend tracking or options — Kubera offers none of those, while tools built for analysis, such as Capitally from €80 a year, do.

Kubera uses standard security — encryption in transit and at rest, plus two-factor authentication — but it is not end-to-end encrypted. Your financial data is readable on Kubera's servers, and account sync runs through third-party aggregators that often require your broker credentials; end-to-end encryption applies only to documents you upload. Capitally takes the opposite approach: everything is encrypted on your device with a key its servers never see.

Kubera tracks current balances, not transactions. It aggregates what each account is worth today and keeps no full transaction ledger, so it cannot reconstruct cost basis or historical returns from source data. Capitally is the opposite — it imports broker statements and records every transaction, which is what defensible tax filings and accurate performance figures depend on.

No. Kubera does not track option contracts or strategies, and it treats dividends as ordinary cash flow with no dividend reports, DRIP handling, withholding-tax tracking or income forecasting. If options or investment income matter to you, Capitally supports full option strategies with Greeks, plus detailed dividend, rental and interest income tracking.

The best Kubera alternative depends on what you need it to do. If you want the same complex-portfolio coverage plus privacy, a full transaction history, tax reporting and deep analytics, Capitally is the closest match for the same audience. If you specifically want automated account aggregation, US-focused tools like Empower are alternatives, though they share Kubera's reliance on third-party aggregators.

You do not migrate data out of Kubera — you import from your brokers instead. Because Kubera stores balances rather than a transaction history, the cleaner path is to export statements from each broker and import them into Capitally, which rebuilds the full history automatically and saves reusable presets for future updates. Real estate, private equity and other off-broker holdings are added as custom assets.

Choose Kubera for a low-maintenance, flat-priced net-worth balance sheet with automated sync, illiquid-asset valuation and estate-handover features. Choose Capitally for on-device end-to-end encryption, a complete transaction history that holds up at tax time, and professional-grade analytics — TWR, MWR, FX attribution, options and multi-jurisdiction tax — across stocks, real estate, private equity and liabilities. Both offer a 14-day trial.