To start investing in dividend stocks, open a brokerage account, pick one of four beginner strategies (dividend ETFs, Dividend Aristocrats, Dogs of the Dow, or a sector mix), buy quality dividend payers, and reinvest payouts via DRIP. Unlike capital gains, dividend payouts arrive on a schedule the company sets — independent of where the share price is trading that quarter. That decoupling is what makes dividends a distinct return stream, not just a flavor of equity exposure.

For beginners, that predictable cash makes investing feel real and rewarding from day one. This guide walks you through everything you need to start: how dividends work, what to look at on a stock, the four simplest strategies, and how to track results over time.

At a glance: 4 dividend strategies for beginners

Strategy | Risk | Time required | Best for |

|---|---|---|---|

Dividend ETFs (e.g. SCHD, VIG, NOBL) | Low | 5 min/year | Total beginners who want one-click diversification |

Dividend Aristocrats (JNJ, PG, KO…) | Low–medium | 1 hr/quarter | Quality-first investors, 25+ year track records |

Dogs of the Dow | Medium | 1 hr/year | Mechanical investors who want a clear rule |

Sector-balanced portfolio | Medium | 2 hr/quarter | Investors who want predictable income across cycles |

You can start any of these with the price of one share (or a fractional share on brokers that support it). The only hard floor is your broker's minimum.

You'll learn:

- How dividend-paying stocks create reliable cash flow

- Which dates matter (declaration, ex-dividend, record, payment) and why

- The 4 metrics that separate quality dividends from yield traps

- How to pick beginner-friendly dividend stocks and ETFs in 2026

- How DRIP (dividend reinvestment) compounds small payments into real wealth

- How to track your portfolio so the strategy actually works

Table of Contents

- At a glance: 4 dividend strategies for beginners

- How does dividend income work?

- The 4 dividend dates every investor must know

- How dividends affect the stock price

- Examples of beginner-friendly dividend stocks and ETFs (2026)

- A worked example, tracked in Capitally

- How to evaluate dividend stocks: 4 metrics every beginner must know

- Dividend yield

- Dividend payout ratio

- Dividend growth rate (DGR)

- Yield on cost

- Other dividend concepts beginners should know

- Different types of dividends

- Dividend Aristocrats and Dividend Kings

- DRIP (Dividend Reinvestment Plan)

- The 4 simplest dividend investing strategies for beginners

- 1. Dividend ETFs: the "set it and forget it" approach

- 2. Dividend Aristocrats: the "quality first" approach

- 3. Dogs of the Dow: the "simple formula" approach

- 4. Sector-balanced approach: the "balanced diet" method

- Key takeaways

- Your next steps

- Frequently asked questions

How does dividend income work?

A dividend is your share of a company's profits, paid out in cash because you own the stock. It is not a gift — it is a distribution to part-owners of the business.

The cycle is simple:

- The company earns profits during a quarter or year

- The board votes to distribute part of those profits to shareholders

- The company announces the dividend amount per share

- Payment is processed on specific dates (see below)

- Shareholders receive cash in their brokerage accounts

Most established US dividend payers run on a quarterly schedule (4 payments per year). Some pay monthly (certain REITs, BDCs, and closed-end funds), and some pay semi-annually or annually (common in Europe).

The 4 dividend dates every investor must know

Four dates govern every dividend. Under today's T+1 settlement cycle, the ex-dividend date for most regular US cash dividends is usually the same day as the record date when the record date falls on a business day. If the record date falls on a weekend or market holiday, the ex-dividend date is usually the previous business day.

- Declaration date — the day the company officially announces the dividend, including the amount, the ex-dividend date, the record date, and the payment date.

- Ex-dividend date — the cutoff. To receive the upcoming dividend, you must buy before the ex-dividend date. If you buy on or after it, the seller gets the dividend.

- Record date — the date the company checks its shareholder register to confirm who is entitled to the payout.

- Payment date — the day the cash arrives in your brokerage account. This can be a few days to a few weeks after the record date.

The ex-dividend date is the critical cutoff

Buy before the ex-dividend date to receive the upcoming dividend. Buy on or after, and you'll need to wait for the next cycle.

Quick example using Apple (AAPL), whose dividend history is published by Apple Investor Relations:

- January 29, 2026 — Apple declared a quarterly $0.26 per share dividend

- February 9, 2026 — record date

- February 9, 2026 — ex-dividend date (same day, because the record date fell on a business day)

- February 12, 2026 — payment date

If you owned 100 shares and bought them before February 9, 2026, you received $26 on February 12. If you bought on or after February 9, the seller got that dividend.

How dividends affect the stock price

The stock price typically opens lower by roughly the dividend amount on the ex-dividend date, because the company has committed that cash to shareholders. In practice, broader market moves can outweigh the effect, so the price may recover quickly — or keep moving for unrelated reasons. It is a normal mechanical adjustment, not automatically a sign of trouble.

Tracking made simple

Tracking ex-dividend dates across multiple stocks gets overwhelming fast. When you import your transactions into Capitally, the platform automatically displays your upcoming dividend payments in a clear calendar view — exactly when each payment arrives, how much you'll receive, and how much will be withheld for tax. You'll never miss an ex-dividend date again.

Examples of beginner-friendly dividend stocks and ETFs (2026)

The simplest beginner portfolios are often built from a small set of widely held, sustainable dividend payers. These are educational examples, not recommendations to buy. Always evaluate valuation, taxes, diversification, and your own goals before investing.

Ticker | Sector | Yield style | Dividend track record | Why it stands out |

|---|---|---|---|---|

JNJ (Johnson & Johnson) | Healthcare | Moderate | 60+ years of increases | Dividend King, defensive cash flow |

PG (Procter & Gamble) | Consumer staples | Low–moderate | 65+ years of increases | Owns brands you buy weekly |

KO (Coca-Cola) | Beverages | Moderate | 60+ years of increases | Global brand, classic income stock |

MCD (McDonald's) | Restaurants | Low–moderate | Nearly 50 years of increases | Long record through multiple recessions |

WMT (Walmart) | Retail | Low | 50+ years of increases | Lower yield, strong dividend growth reputation |

SCHD (Schwab US Dividend ETF) | ETF | Higher-income ETF | Dividend-quality screen | One-fund US dividend exposure, low fee |

VIG (Vanguard Dividend Appreciation ETF) | ETF | Lower-yield, growth-oriented ETF | Dividend-growth focus | Broad diversification, low fee |

For European investors who can't trade US ETFs directly, look at UCITS equivalents like VHYL (Vanguard FTSE All-World High Dividend Yield UCITS) and SPYD on Xetra (SPDR S&P US Dividend Aristocrats UCITS) — same dividend-focused exposure in a UCITS wrapper.

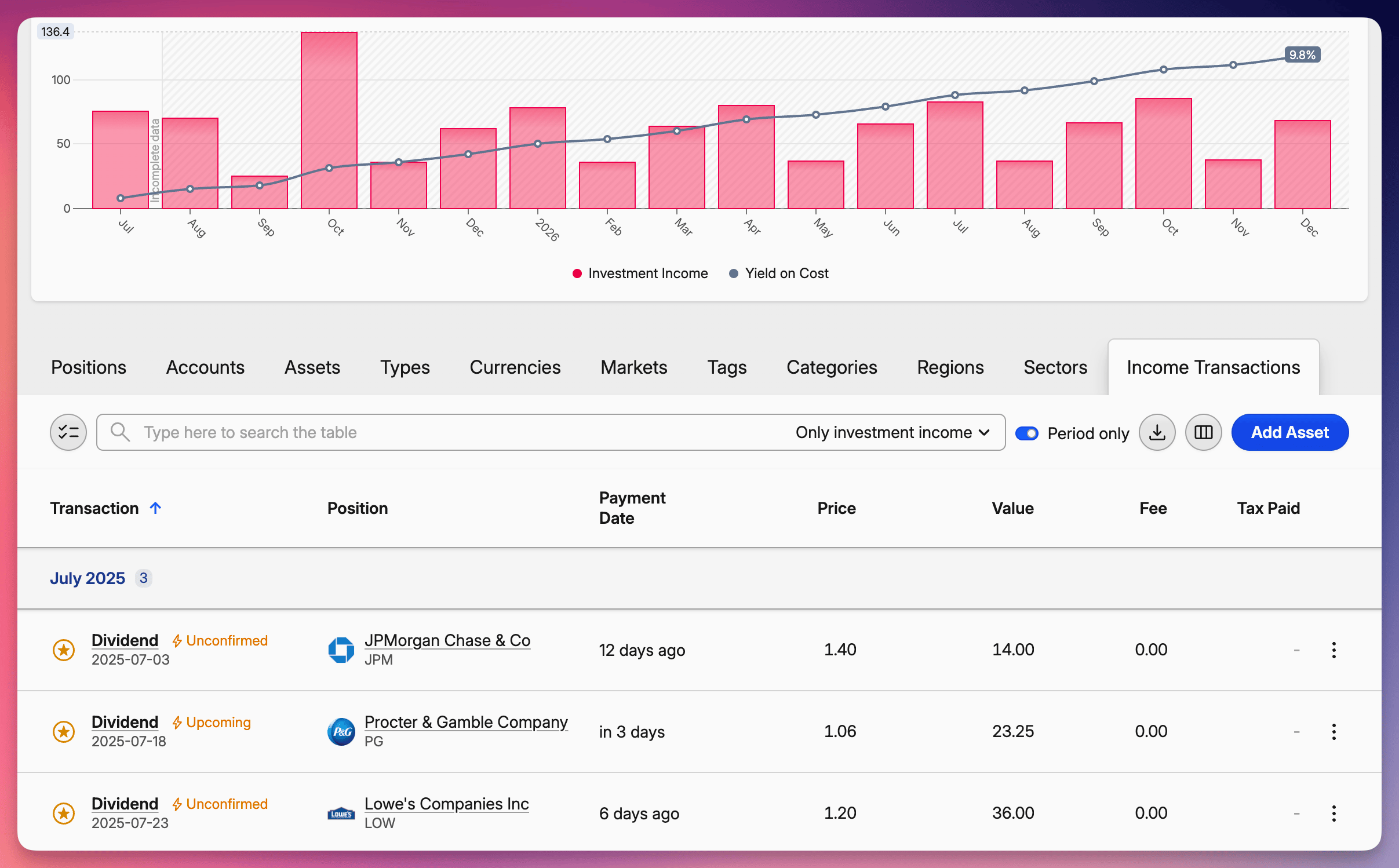

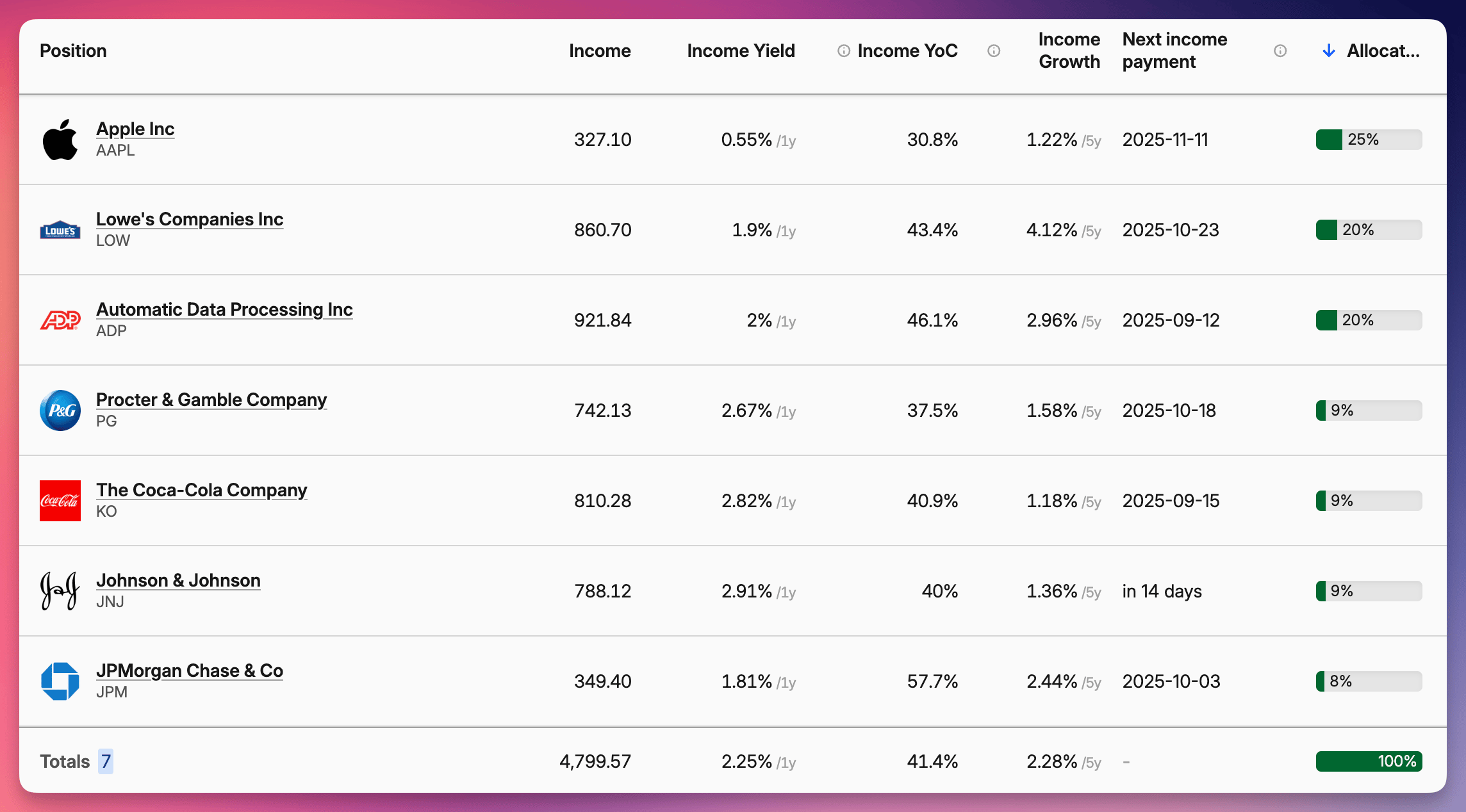

A worked example, tracked in Capitally

The screenshot below shows what a beginner portfolio of five Aristocrats actually did — $2,000 bought of each on January 5, 2015 (Johnson & Johnson, Procter & Gamble, Coca-Cola, Lowe's, ADP) and held without trading. The view breaks total return into capital gains and dividend income side by side.

Total returns of this portfolio as displayed by Capitally

Total returns of this portfolio as displayed by CapitallyThe dividend portion is what a price-only chart hides. With reinvestment, that bar grows further still — each payout buys more shares that generate more payouts, year after year.

How to evaluate dividend stocks: 4 metrics every beginner must know

Picking a quality dividend stock isn't about chasing the highest yield. It's about finding businesses that can sustain and grow their dividends through full economic cycles. Four metrics tell you most of what you need to know — for the full deep dive, see the complete dividend metrics guide.

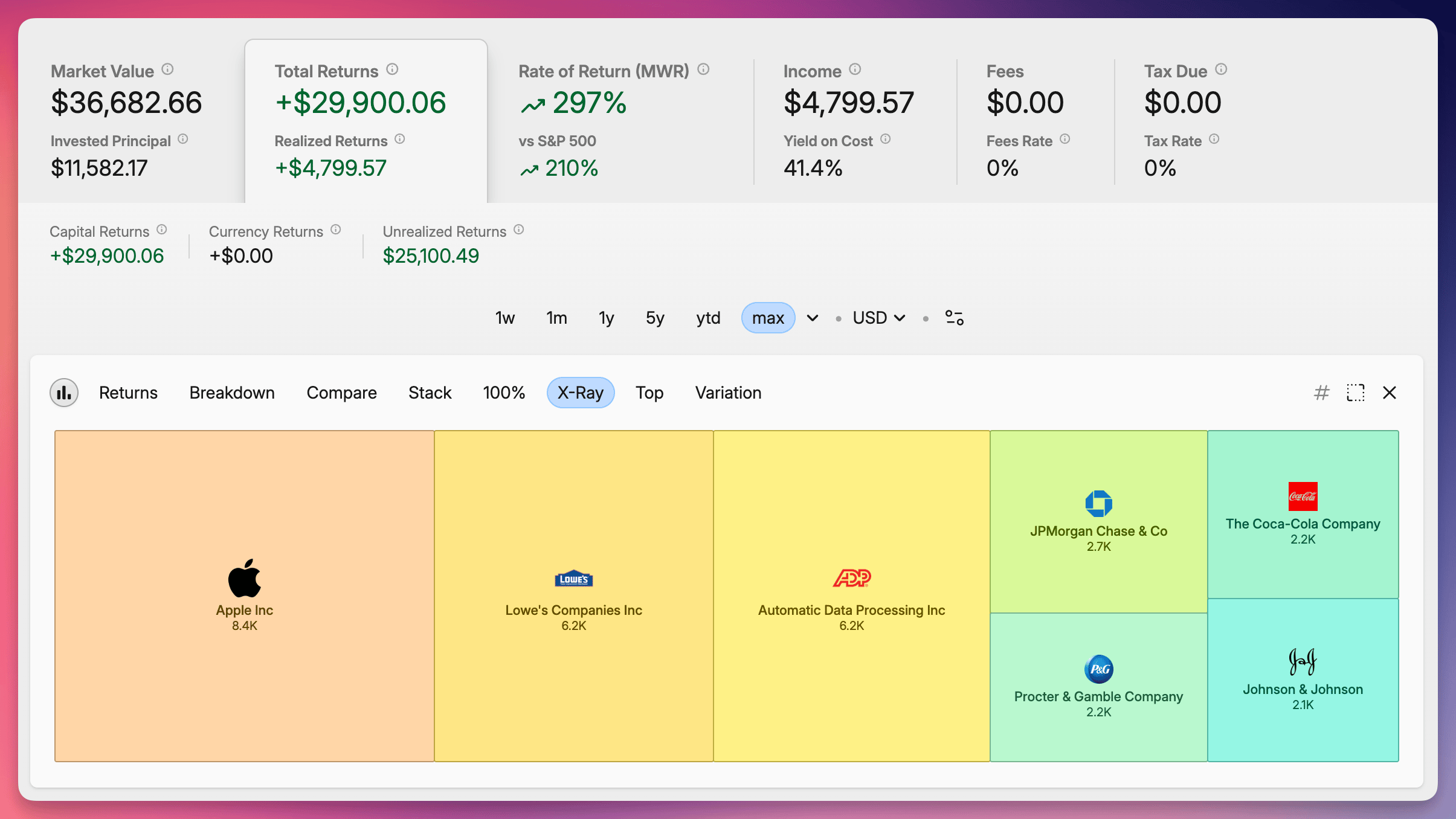

Dividend yield

Assets paying the highest yield as displayed by Capitally

Assets paying the highest yield as displayed by CapitallyDividend yield = Annual Dividend per Share ÷ Current Share Price × 100%

It tells you how much income a stock produces relative to its current price. A $50 stock paying $2 in annual dividends has a 4% yield. Useful for quick comparison — but a yield much higher than the company's history or its industry peers usually signals a falling stock price, not a generous company.

When a stock's yield suddenly jumps far above its historical average or industry peers, it's almost always because the price fell — not because the company became more generous. This is called a yield trap.

Dividend payout ratio

Payout ratio = Annual Dividend per Share ÷ Annual Earnings per Share × 100%

Shows what share of earnings is being paid out as dividends. Lower is generally safer. For most industries a payout ratio under 60% leaves room to keep paying even if profits dip. Utilities and REITs run higher (70–90%) by design; tech and consumer goods companies typically run 30–50%.

Dividend growth rate (DGR)

DGR = ((Current Annual Dividend ÷ Dividend N years ago)^(1/N) − 1) × 100%

Companies that consistently grow dividends typically outperform those with flat payouts. A 5–10% annual DGR is a strong signal of a healthy business.

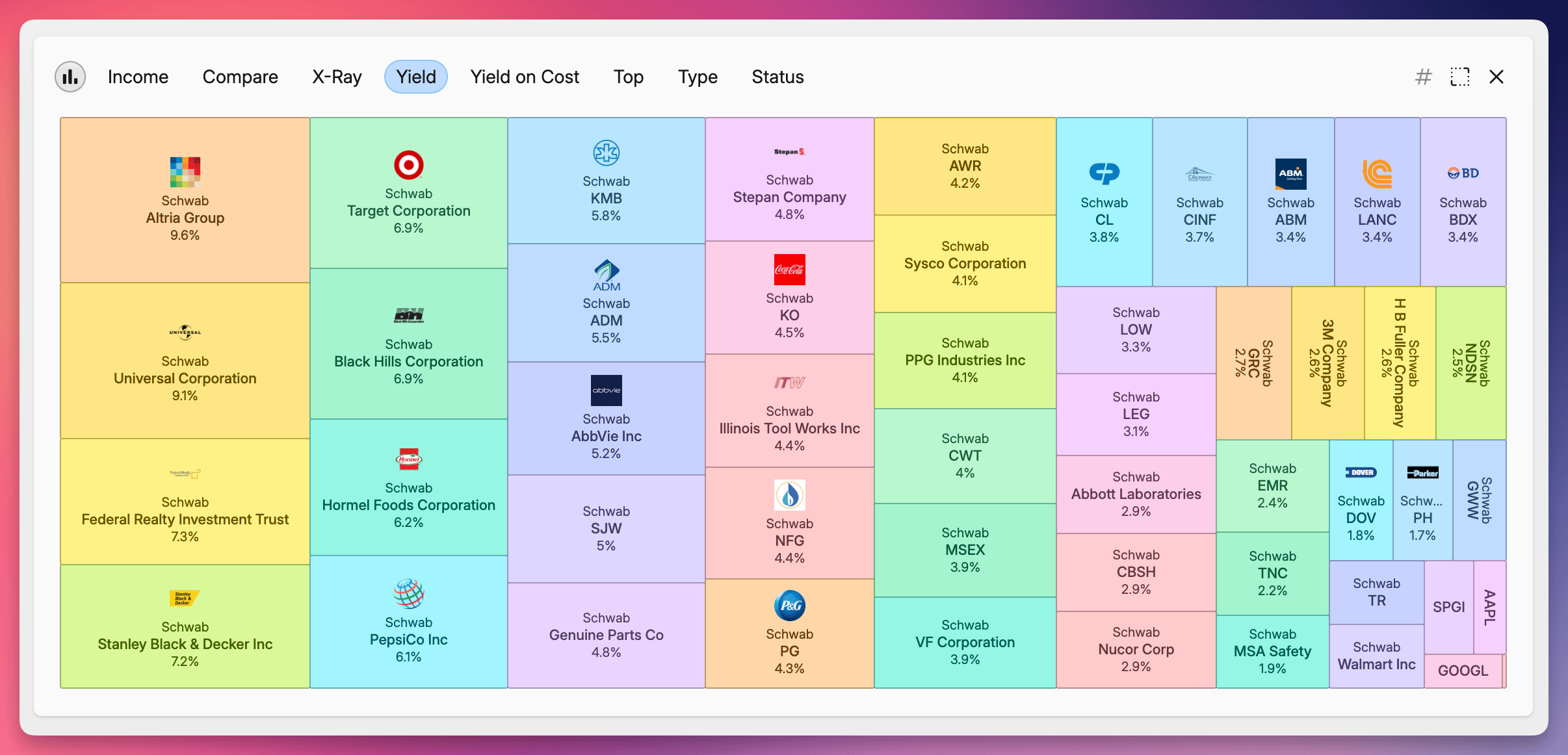

Yield on cost

Yield on cost = Current Annual Dividend per Share ÷ Your Purchase Price per Share × 100%

Your personal yield based on what you paid, not today's price. Long-term dividend investors often end up with yields on cost far above the market's current yield — that's compounding doing its work.

Track your real yield

Yield on Cost & Yield compared in Capitally

Yield on Cost & Yield compared in CapitallyYield on cost gets messy when you've bought shares at different prices over the years. Capitally automatically calculates your true yield on cost across every purchase of a stock, so you see your actual dividend return based on your specific investment history — not a textbook number.

Other dividend concepts beginners should know

Different types of dividends

Tax treatment depends on your country and account type. The notes below are simplified educational examples, not tax advice.

Not every dividend is the same. The four types you'll encounter:

- Regular cash dividends — the standard. Cash deposited to your brokerage every quarter (or month/half-year). The foundation of any beginner portfolio.

- Special dividends — one-time bonus payments outside the regular schedule, usually from exceptional profits, asset sales, or restructuring. Microsoft's $3/share special dividend in 2004 returned $32 billion to shareholders. Nice when they happen, but unpredictable — don't plan income around them.

- Stock dividends — additional shares instead of cash. A 5% stock dividend means 5 new shares for every 100 you own. Tax treatment varies by country; in many cases tax is deferred until sale, but not always.

- Return of capital — when part of the "dividend" is actually returning your own money (common in REITs, MLPs, and some funds). Tax treatment varies, but it often reduces your cost basis and can increase future capital gains tax.

Beginners should focus almost entirely on regular cash dividends from companies with consistent histories.

Dividend Aristocrats and Dividend Kings

These aren't metrics — they're elite categories.

- Dividend Aristocrats — S&P 500 companies that have raised their dividend for at least 25 consecutive years, per S&P Dow Jones Indices' official methodology.

- Dividend Kings — companies that have raised their dividend for at least 50 consecutive years (no S&P 500 requirement).

These businesses have grown payouts through multiple recessions, market crashes, and full economic cycles. They form the backbone of many dividend portfolios.

DRIP (Dividend Reinvestment Plan)

A DRIP automatically uses your dividends to buy more shares of the same stock — often commission-free, often in fractional shares. Reinvested dividends generate more dividends, which buy more shares, and so on. Over decades, the compounding effect can transform a modest portfolio into real wealth.

Quick example: 100 shares of a $50 stock with a 4% yield pays $200 a year. With DRIP, that $200 buys 4 more shares — so next year you collect $208, then $216, then $225, and the curve keeps steepening.

The 4 simplest dividend investing strategies for beginners

The most effective beginner strategies are also the simplest. Pick one — or combine two — and stick with it.

1. Dividend ETFs: the "set it and forget it" approach

Quick summary: Buy one fund, get instant diversification across hundreds of dividend payers. Lowest effort, lowest single-stock risk, perfect first step.

How it works: you buy shares of an ETF (Exchange Traded Fund) that focuses on dividend-paying stocks. The fund manager handles the picking and rebalancing. You buy one ticker, you own dozens or hundreds of dividend stocks behind the scenes.

Why it works for beginners:

- Instant diversification across many companies

- Professional portfolio management

- Lower risk than picking individual stocks

- Low fees (often <0.1% per year for the big ones)

- Can start with the price of one share — typically $50–150

Accumulating vs distributing ETFs:

- Accumulating ETFs automatically reinvest distributions inside the fund. In some countries that can defer current tax, while in others investors may still owe tax each year even though no cash is paid out.

- Distributing ETFs pay cash to your brokerage account on a schedule. You see the cash flow directly, and taxation depends on your country and account type.

Many ETFs come in both versions — pick based on whether you want the cash now or want to maximize compounding.

Aristocrat-focused ETFs to know:

- NOBL — ProShares S&P 500 Dividend Aristocrats ETF (only stocks with 25+ year streaks)

- SDY — SPDR S&P Dividend ETF (S&P High Yield Dividend Aristocrats Index, 20+ years)

- VIG — Vanguard Dividend Appreciation ETF (broad dividend-growth focus)

- SCHD — Schwab US Dividend Equity ETF (high-quality high-yield US dividend payers, very popular)

ETFs for European investors

Europeans can only buy UCITS-compliant ETFs. Many US ETFs have a UCITS twin (often with a different ticker), but composition, currency, and tax treatment can differ. Look for VHYL (Vanguard FTSE All-World High Dividend Yield UCITS), SPYD (SPDR S&P US Dividend Aristocrats UCITS), or FUSD (Fidelity US Quality Income UCITS).

How to start: open a brokerage account → pick 1–2 ETFs from the list above → set up an automatic monthly purchase. That's it.

Watch out for high-yield ETFs (YieldMax, covered call funds)

A separate breed of "dividend" ETFs uses options strategies to manufacture income. The YieldMax family (TSLY, APLY, NVDY) sells covered calls on a single stock to produce monthly income with yields sometimes above 20%.

They look incredible on paper — and badly underperform in strong bull markets, because the call options cap upside while the underlying stock keeps running. They're income tools for retirees, not wealth-building tools for beginners with long time horizons.

Rule of thumb: if the yield is over 10% and you don't understand exactly where it comes from, treat it with extreme caution.

2. Dividend Aristocrats: the "quality first" approach

Quick summary: Build a small portfolio of companies that have raised dividends every single year for at least 25 years — through recessions, pandemics, and crashes. Higher effort than ETFs, deeper conviction in each holding.

How it works: instead of chasing the latest tech trend, you build a basket of companies with proven histories of raising dividends. A Dividend Aristocrat is an S&P 500 company that has increased its dividend for at least 25 consecutive years. A Dividend King has done it for 50+ years.

Some of these companies were raising payments to shareholders through Nixon's resignation, the 1987 crash, the dot-com bust, and the 2008 financial crisis. That kind of streak is hard to fake.

Why it works for beginners:

- Like riding with an experienced driver — fewer accidents (read: dividend cuts)

- Survivors of multiple major recessions

- Defensive businesses selling everyday products (toothpaste, medicine, food)

- Historically outperformed the broader market with less volatility

Stock price alone is only half the story

A flashy non-dividend stock might gain 80% over a decade. A "boring" dividend payer might gain only 40% over the same window. Who won?

The answer isn't obvious. With a 4% dividend yield reinvested annually, the dividend stock's total return after 10 years can close most of that gap — and over longer horizons (20+ years) it routinely overtakes the price-only chart. Dividends compound silently, and most charts show only price.

Johnson & Johnson over 2010–2020 is a classic example: the share price more than doubled, and reinvesting the dividends along the way added roughly another 50 percentage points to the total return. Skip dividends in your mental model and you under-count what dividend stocks actually deliver.

How to pick quality Aristocrats and Kings:

- Payout ratio — what share of earnings goes to dividends? Below 60% is the safe zone for most industries.

- Dividend growth rate — would you rather take a steady 5–10% raise every year, or get nothing for four years and then 50%? Steady wins.

- Financial health — low debt, healthy cash reserves. The difference between a friend with savings and one always asking for loans.

- Competitive moat — does the company have something competitors can't replicate? Coca-Cola has its brand, Apple has its ecosystem, Johnson & Johnson has thousands of patents.

The power of reinvestment

Start with $10,000 in a basket of Aristocrats yielding 3%. Year one, you collect ~$300 — not life-changing. But reinvest it, let the underlying companies raise their dividend ~7% a year (typical for Aristocrats), and after 30 years your $10,000 turns into over $100,000 — even with very modest stock price appreciation. Compounding does the heavy lifting.

Aristocrat / King names worth knowing (full lists maintained by S&P Dow Jones Indices and Sure Dividend):

- JNJ — Johnson & Johnson (60+ years, healthcare King)

- PG — Procter & Gamble (65+ years, consumer staples King)

- KO — Coca-Cola (60+ years, beverages King)

- MCD — McDonald's (approaching 50 years)

- WMT — Walmart (50+ years, King)

- CLX — Clorox (50+ years, King)

- ADP — Automatic Data Processing (50+ years, King)

- LOW — Lowe's (60+ years, King)

Outside the US:

- UL — Unilever (UK-domiciled consumer goods giant; brands include Dove, Vaseline, Axe/Lynx, Rexona, TRESemmé)

- NVS — Novartis (Swiss pharma, 29 consecutive years of dividend growth)

- RY — Royal Bank of Canada (paid dividends every year since 1870; held its dividend through 2008 when many US banks cut)

Picking individual aristocrats too daunting?

You're not alone. The r/dividends subreddit is the most active community for this — thousands of investors post portfolios, mistakes, and tradeoffs. Nobody there is going to do the picking for you, but reading how others build is one of the fastest ways to calibrate.

You can also use Capitally to show your portfolio to others.

You can also use Capitally to show your portfolio to others.3. Dogs of the Dow: the "simple formula" approach

Quick summary: Once a year, buy the 10 highest-yielding stocks in the Dow. Hold one year. Rebalance. That's it. Mechanical, no judgment calls.

How it works:

- On January 1st, identify the 10 Dow Jones stocks with the highest dividend yields

- Invest equal amounts in each

- Hold for one year

- Rebalance the next January 1st: sell the ones no longer in the top 10, buy the new entrants

Why it works for beginners:

- Mechanical rules — no judgment calls

- Only requires attention once per year

- Focuses on large, established companies

- Naturally rotates into stocks that may be temporarily undervalued (yields rise when prices fall)

Dogs of the Dow can concentrate heavily in a couple of sectors when those sectors are out of favor. Check sector exposure once a year — if it's lopsided, that's a feature of this strategy, not a bug, but you should know.

4. Sector-balanced approach: the "balanced diet" method

Quick summary: Spread holdings across 5 economic sectors with different dividend profiles, so your income survives any single sector's bad year.

How it works: build a portfolio with dividend stocks from multiple sectors, recognizing that different industries have different dividend profiles.

Sample 5-sector starter portfolio:

Sector | Example | Yield profile | Growth profile |

|---|---|---|---|

Utilities | NextEra Energy (NEE) | Higher | Slower |

Consumer staples | Procter & Gamble (PG) | Moderate | Steady |

Healthcare | Johnson & Johnson (JNJ) | Lower | Reliable |

Financials | JPMorgan Chase (JPM) | Variable | Cyclical |

Technology | Microsoft (MSFT) | Lower | Highest growth |

Why this works: sectors react differently to economic conditions. Utilities hold up when growth fades, financials thrive when rates rise, tech leads when investors get optimistic. Spreading across them keeps your income stream steady through full cycles.

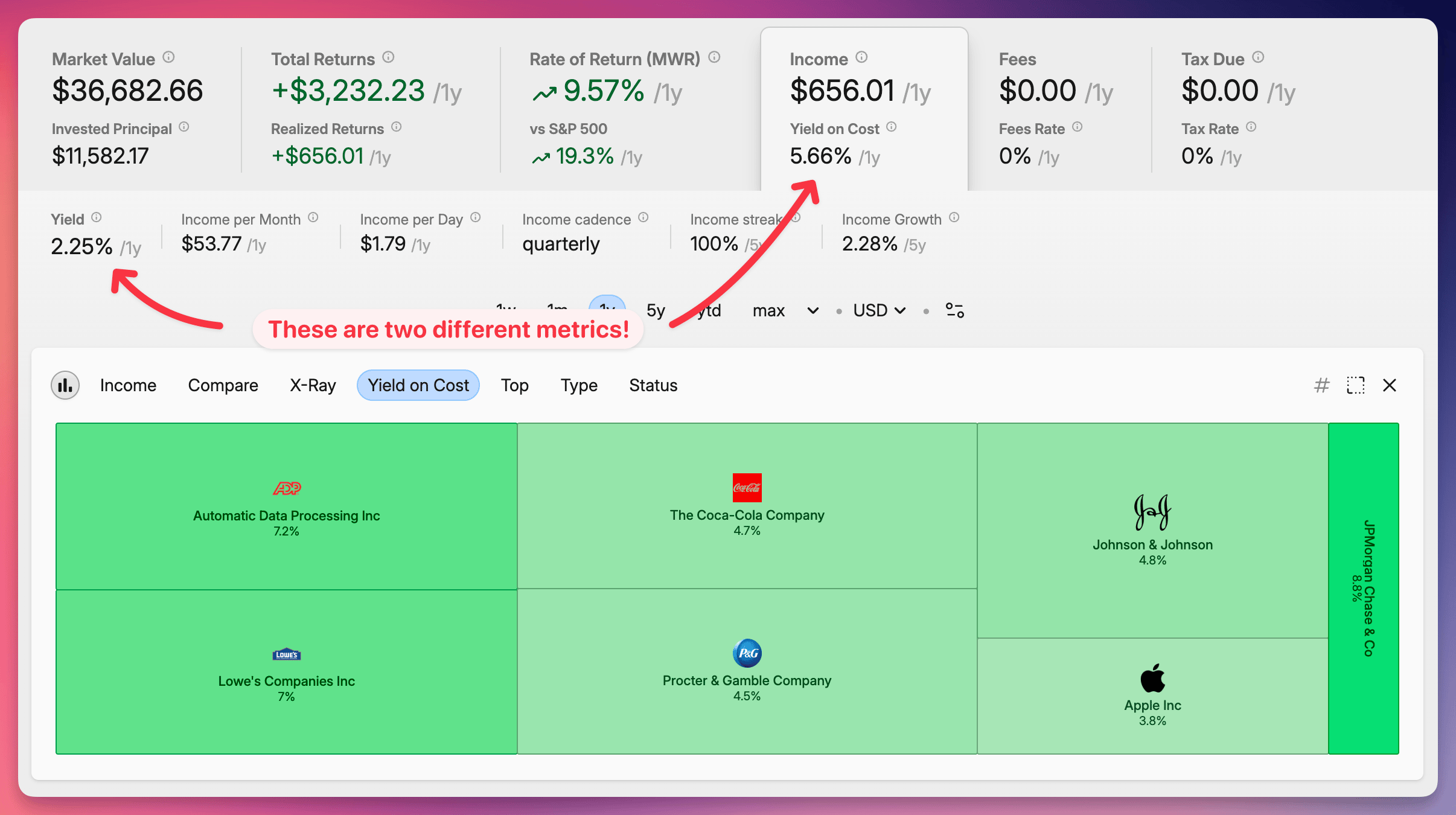

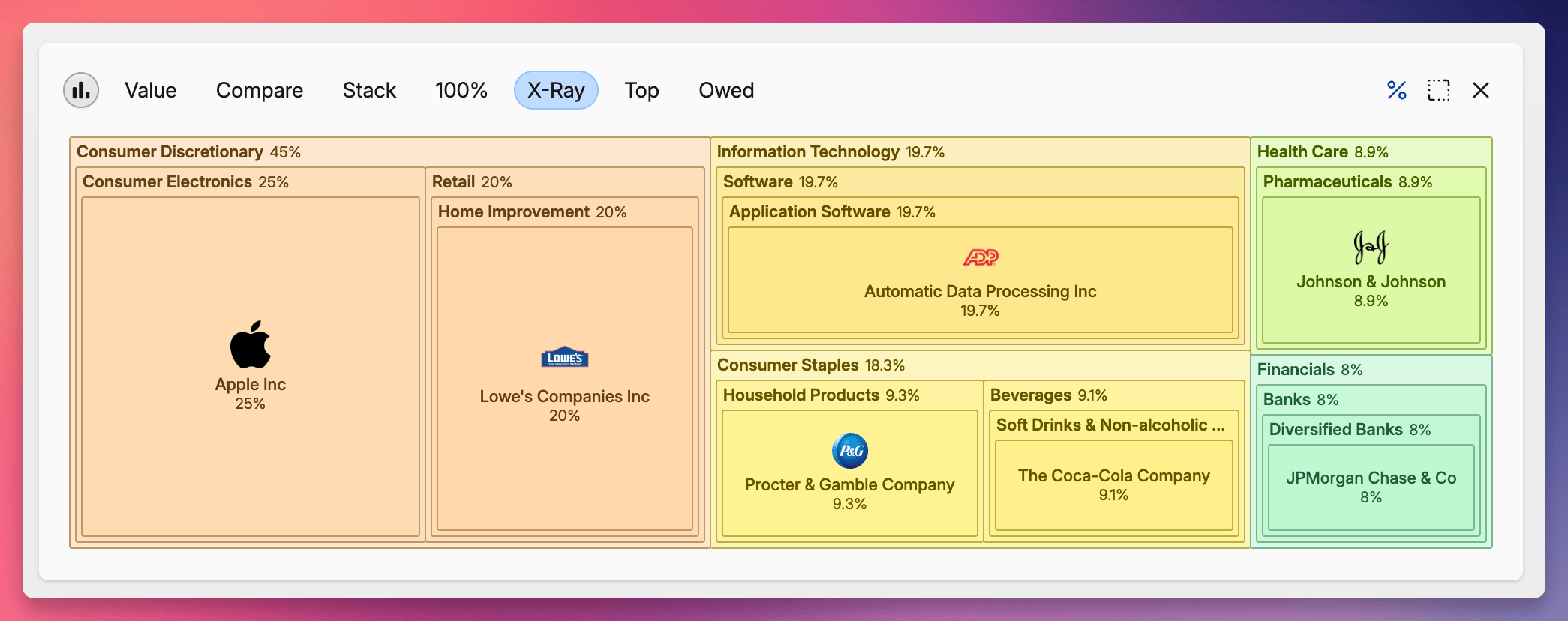

Check your sector allocation

As your portfolio grows, sector exposure becomes the single most-overlooked source of risk.

Detailed sector allocation as displayed by Capitally

Detailed sector allocation as displayed by CapitallyCapitally automatically categorizes every holding by sector and shows where your dividend income is actually coming from. If one sector is quietly producing 60% of your income, you'll see it before the next downturn does.

Key takeaways

- Dividend quality matters more than yield alone. Focus on payout ratio, growth, and business fundamentals — not just the headline number.

- For beginners, regular cash dividends from established companies are the only category that matters. Skip special dividends, stock dividends, and exotic high-yield ETFs at the start.

- Pick one strategy (or combine two): dividend ETFs for one-click exposure, Aristocrats for quality, Dogs of the Dow for a mechanical rule, sector mix for balanced income.

- Reinvest your dividends. DRIP turns ordinary cash payments into compound growth and can materially increase long-term total return.

- Track everything. Without a clear view of yield, yield on cost, payout ratio, and sector exposure, the strategy becomes harder to manage over time. Spreadsheets also get harder to maintain as portfolios grow.

Dividend investing combines capital appreciation with predictable income — a rare combination for long-term wealth building. Pick a strategy, reinvest, give it years, and compounding does much of the work.

Your next steps

- Open a brokerage account if you don't have one

- Pick one strategy from above (most beginners do best with a dividend ETF + 3–5 Aristocrats)

- Set up automatic monthly contributions

- Enable DRIP, or buy an accumulating UCITS ETF if you're in Europe

- Read the dividend metrics deep dive to evaluate any individual stock you're considering

- Set up dividend tracking — see how to track dividends for spreadsheet vs broker vs dedicated tracker comparison

- Check sector allocation once a quarter

The best time to plant a dividend tree was twenty years ago. The second best time is today.

Frequently asked questions

To live off dividends, you typically need a portfolio that generates enough annual dividend income to cover your expenses — at a 3.5% portfolio yield, that's roughly $28–30 of portfolio per $1 of annual spending. For $40,000 a year of dividend income, plan on a portfolio around $1.1–1.3 million. The exact number depends on your yield, tax situation, and whether you also draw on price appreciation.

Yes — for most beginners, dividend stocks are a strong starting point. They produce visible cash payments, force you to focus on quality businesses, and often show lower volatility than the broader market, especially when compared with speculative growth stocks. They are not always the highest-return strategy in raging bull markets, but they are one of the most beginner-friendly ways to learn investing without panicking on the first downturn.

The most-recommended beginner dividend ETFs are SCHD (Schwab US Dividend Equity, US-focused), VIG (Vanguard Dividend Appreciation, growth tilt), NOBL (ProShares S&P 500 Dividend Aristocrats), and SDY (SPDR S&P Dividend). European investors should look at the UCITS equivalents like VHYL and SPYD.

Most US dividend stocks pay quarterly (4 times a year). Some REITs and BDCs pay monthly. Many European stocks pay semi-annually or annually. ETFs distribute on a fixed schedule (often quarterly) — accumulating ETFs reinvest internally instead of paying out.

Reinvest while you're building wealth; take cash once dividends are funding your lifestyle. Reinvested dividends compound: the same $10,000 invested over 30 years at a 4% dividend yield ends at roughly $32,400 with reinvestment vs $22,000 if you take the cash — a 47% difference. A DRIP (Dividend Reinvestment Plan) automates this.

Yes, but it requires capital. At a 3.5% portfolio yield, $1,000 per month ($12,000 a year) of dividends needs roughly $340,000 invested. At a 5% yield (with somewhat higher risk), the figure drops to around $240,000. Reinvest dividends along the way and the number you actually need to put in is significantly less.

In the US, qualified dividends are taxed at the long-term capital gains rate (0%, 15%, or 20% depending on income) — much lower than ordinary income tax. To qualify you must hold the stock for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date, and the stock must be from a US corporation or qualifying foreign corporation. Ordinary (non-qualified) dividends include most REIT distributions and are taxed as regular income.

Many companies — especially young, fast-growing ones (think tech and biotech) — choose to reinvest all their earnings back into the business instead of paying dividends. The bet is that capital appreciation will outpace what shareholders would earn from dividends. Amazon, Google, and Berkshire Hathaway famously didn't pay dividends for decades. The trade-off: no regular income, but potentially much higher long-term returns if the bet works.

The board of directors votes on each dividend after reviewing earnings, cash flow, future investment needs, and dividend history. Most established payers target a specific payout ratio (often 30–60% of profits) and aim for steady, gradual growth rather than dramatic changes — because cutting a dividend is one of the worst signals a public company can send.

Compound interest earns returns on both your original investment and on previous returns. For dividend investors, taking dividends as cash is simple interest; reinvesting dividends is compound interest. Example: $10,000 invested at a 4% dividend yield over 30 years grows to about $22,000 if you take dividends as cash ($10,000 original + $12,000 collected), or about $32,400 if you reinvest — 47% more. The longer you stay invested, the bigger the gap.

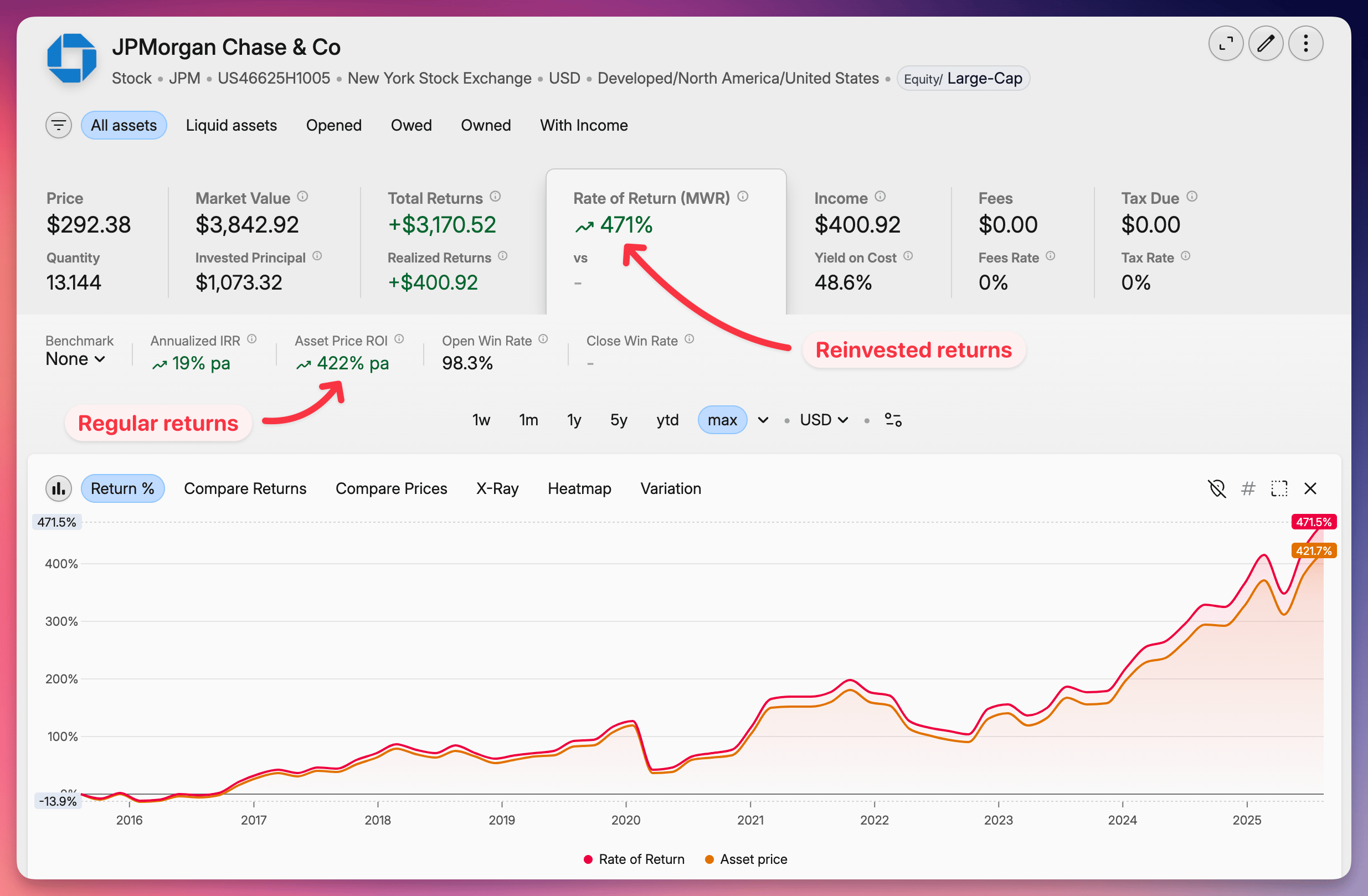

Reinvest your dividends!

Those impressive market return numbers in financial charts? They assume reinvestment. But dividends don't reinvest themselves — they sit as cash unless you act.

For hassle-free compounding, set up a Dividend Reinvestment Plan (DRIP) with your broker. DRIPs buy more shares automatically every time a dividend is paid, usually commission-free. Fidelity, Schwab, and Vanguard all support it with one setting. An accumulating UCITS ETF can play a similar compounding role to a DRIP, though the tax outcome may differ by country.

Difference in returns between paid out and reinvested dividends in Capitally

Difference in returns between paid out and reinvested dividends in Capitally